← Work

Tree-Nation

Payment Infrastructure

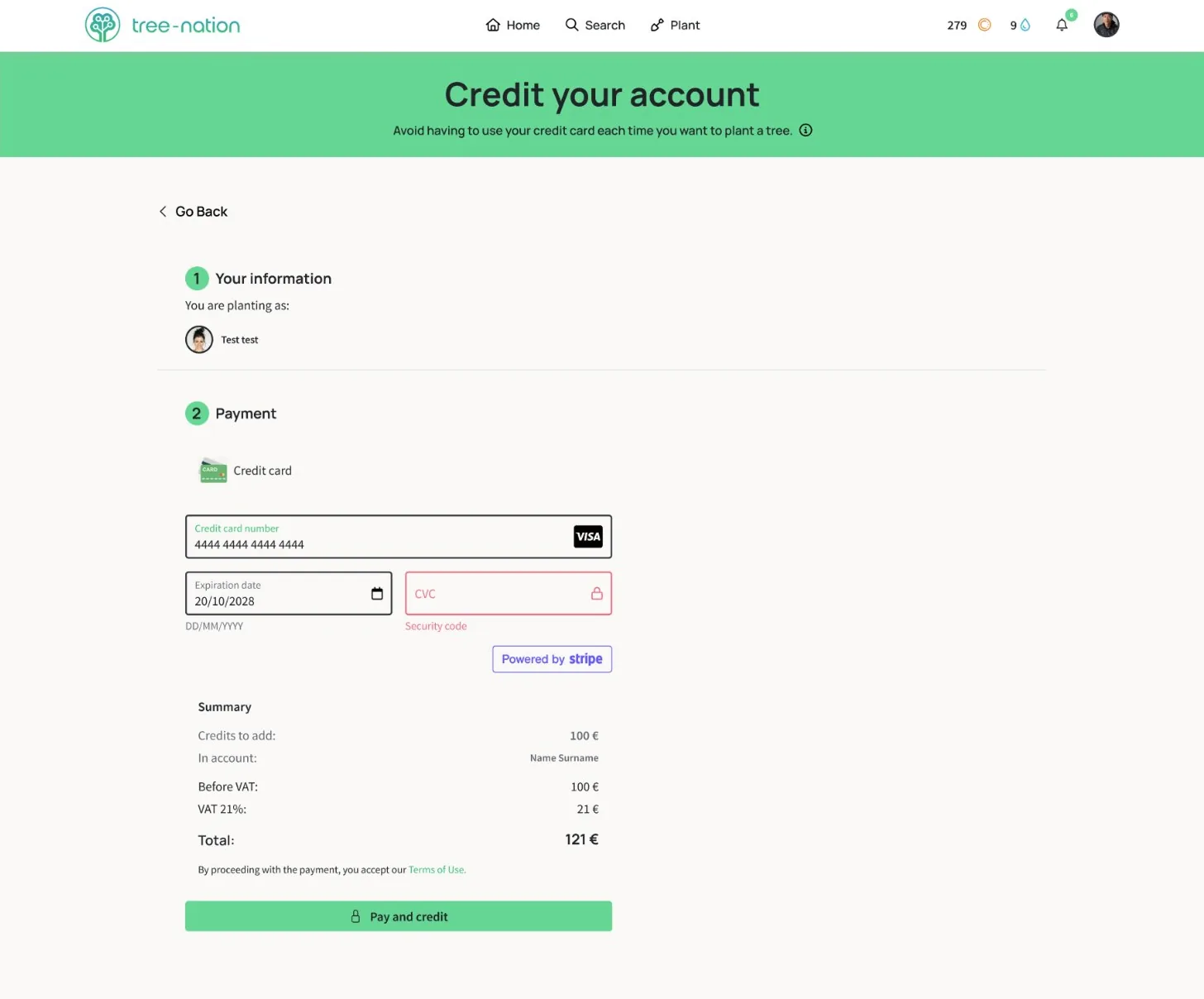

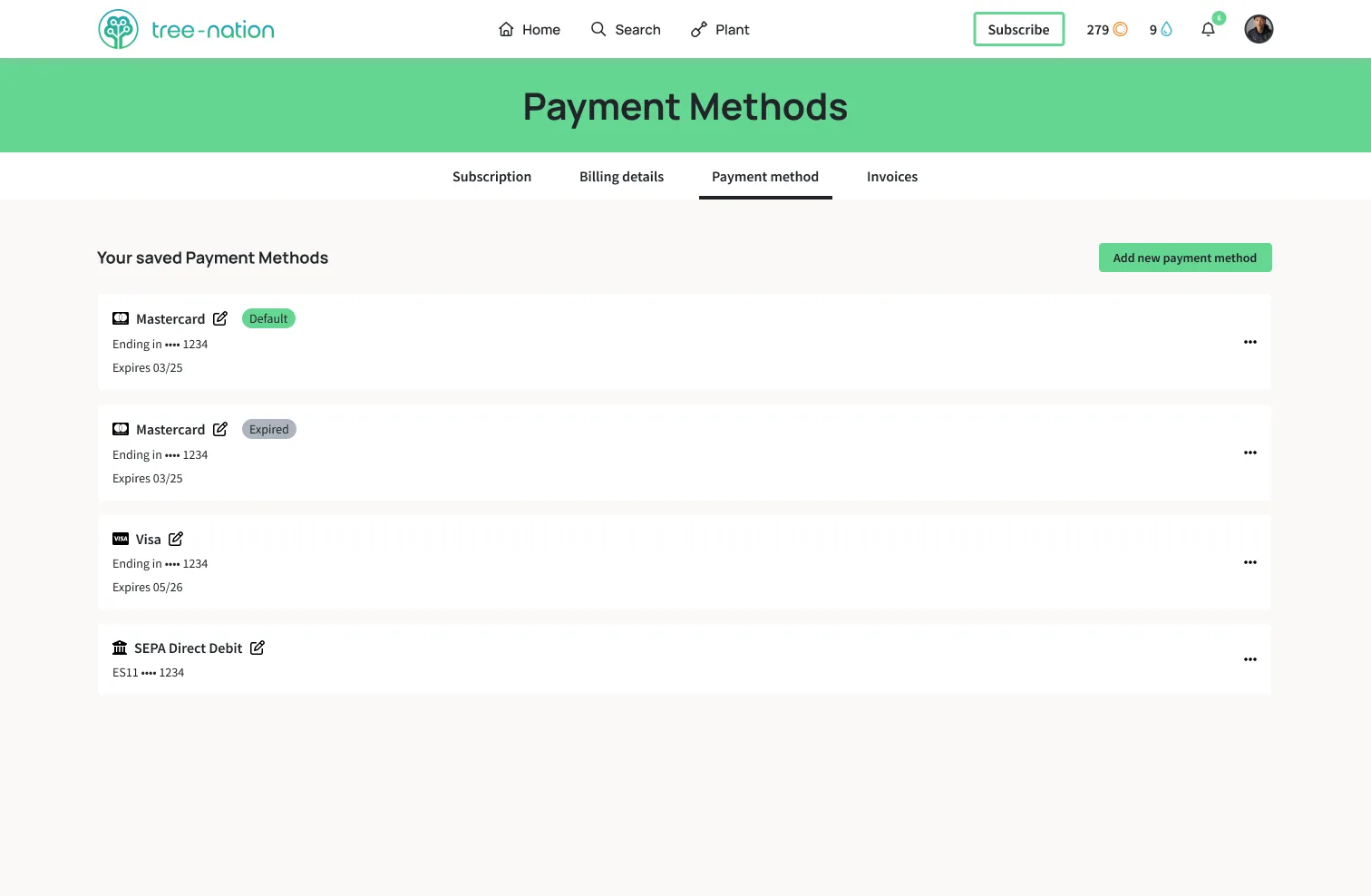

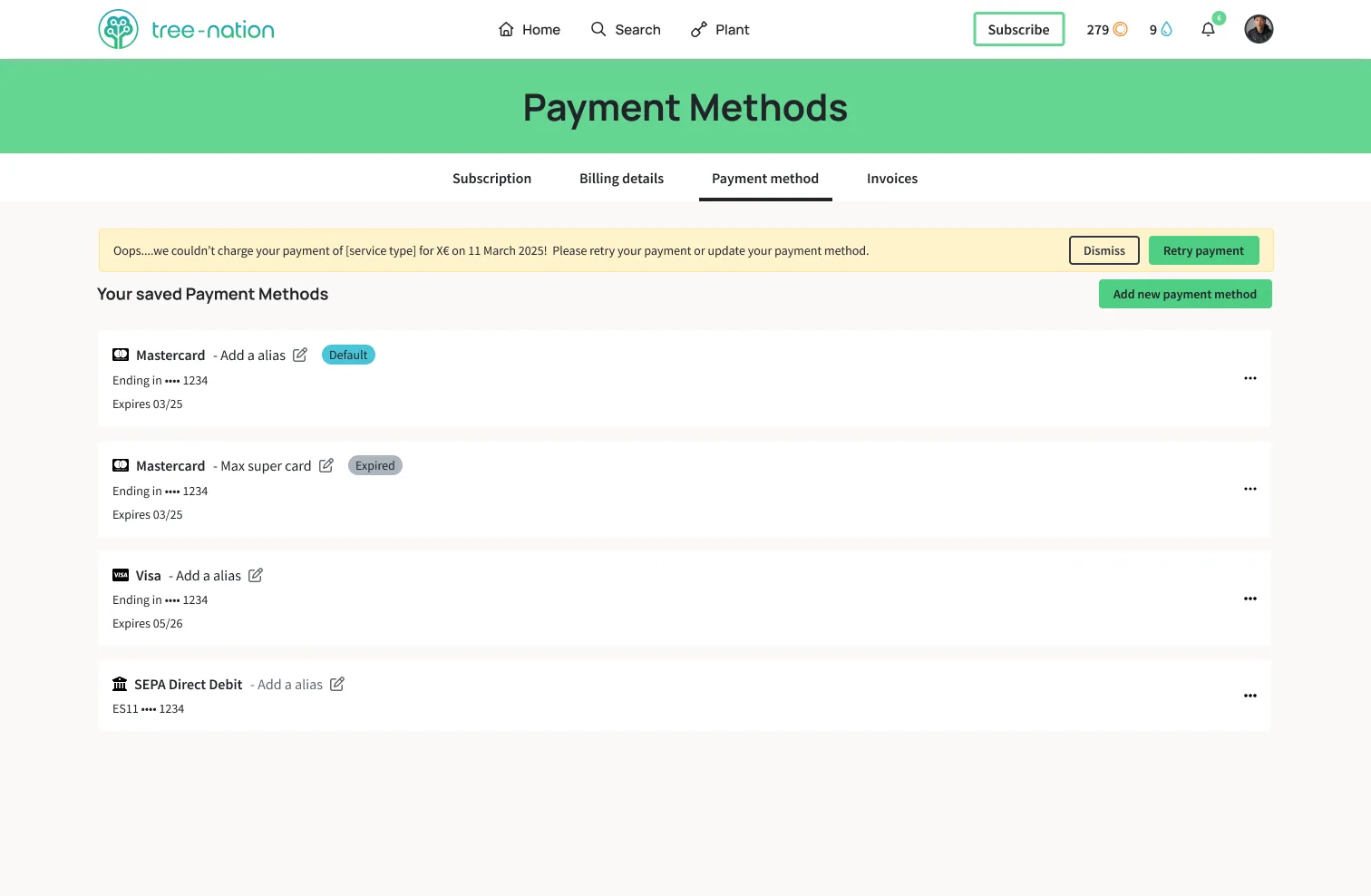

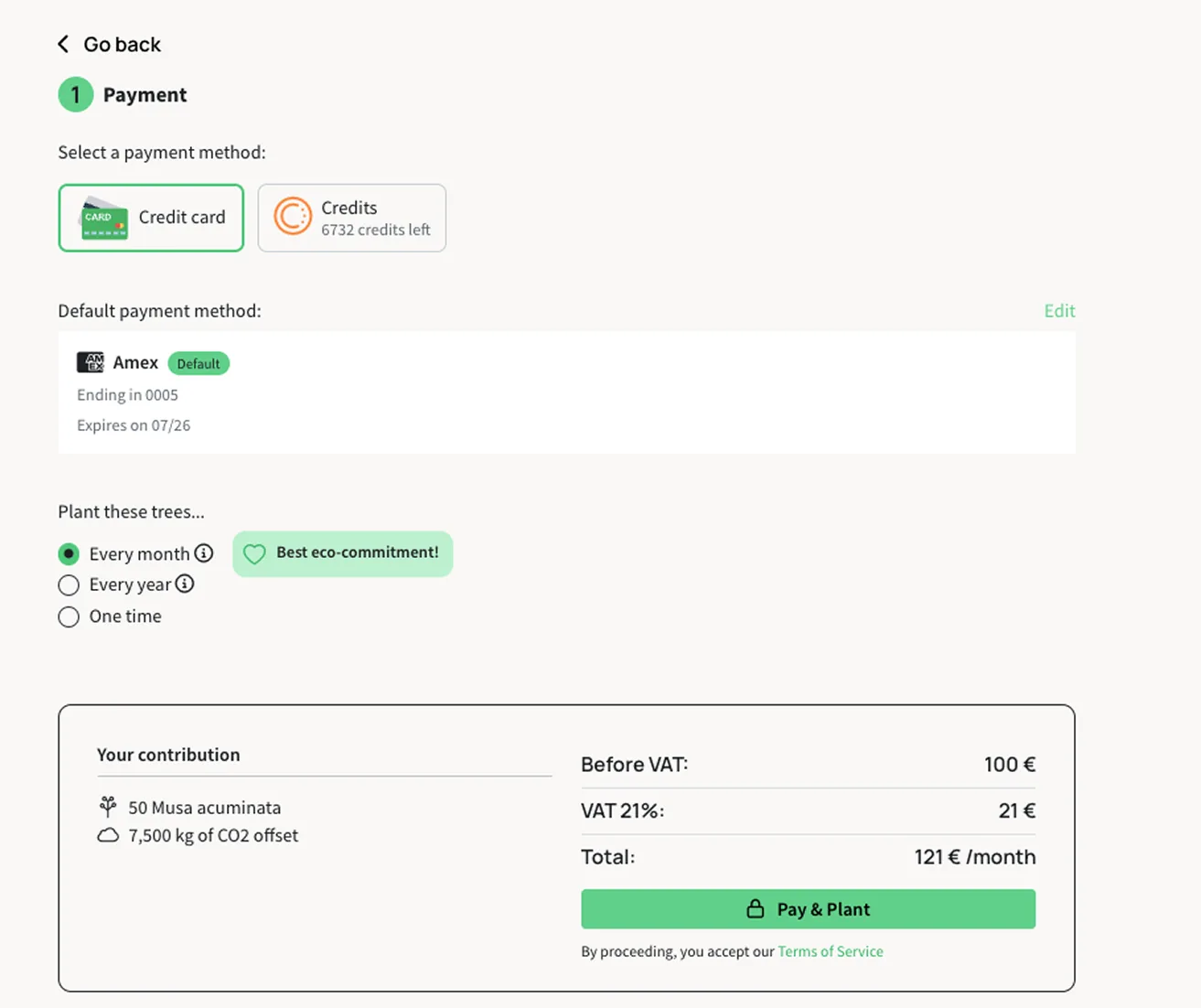

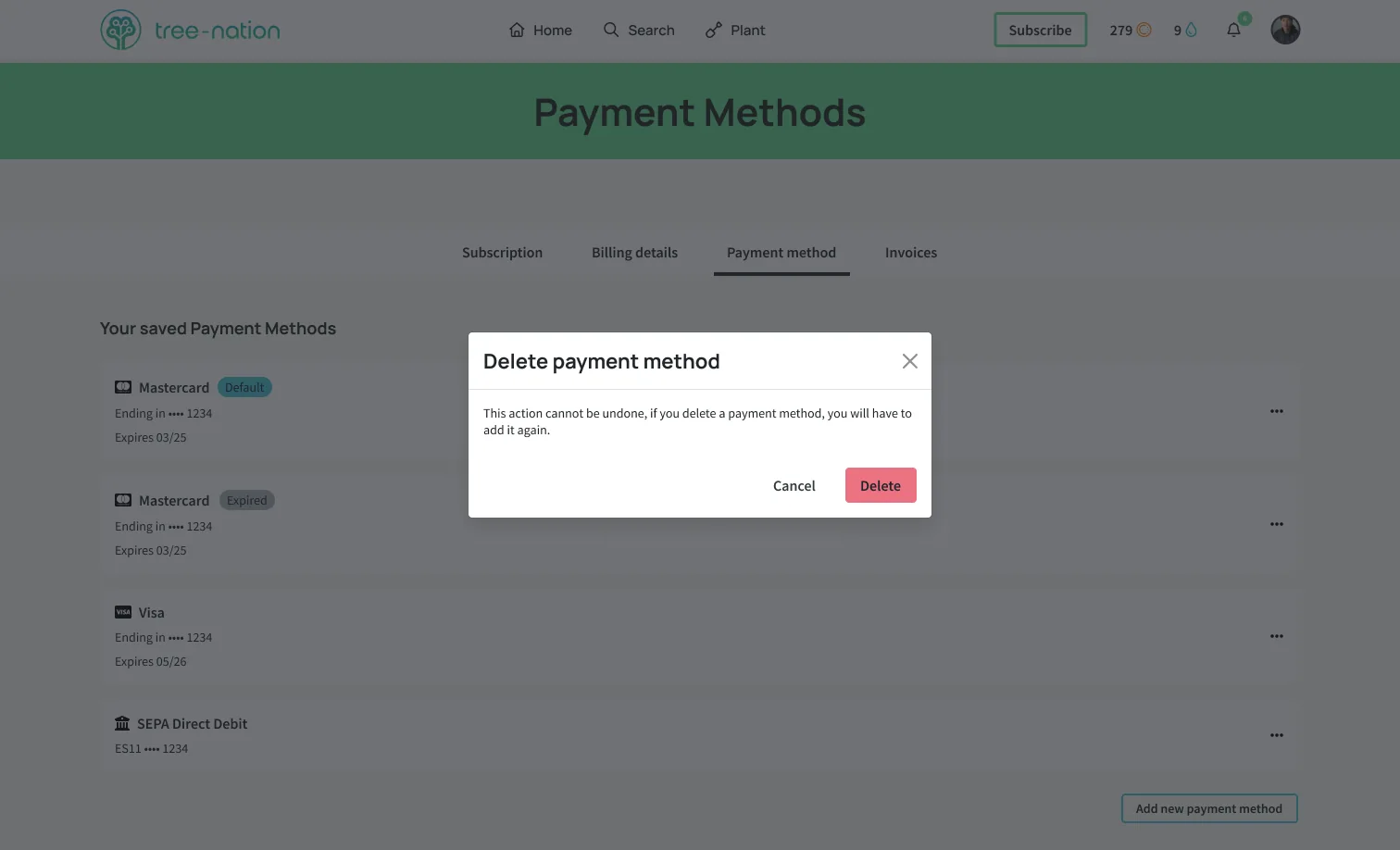

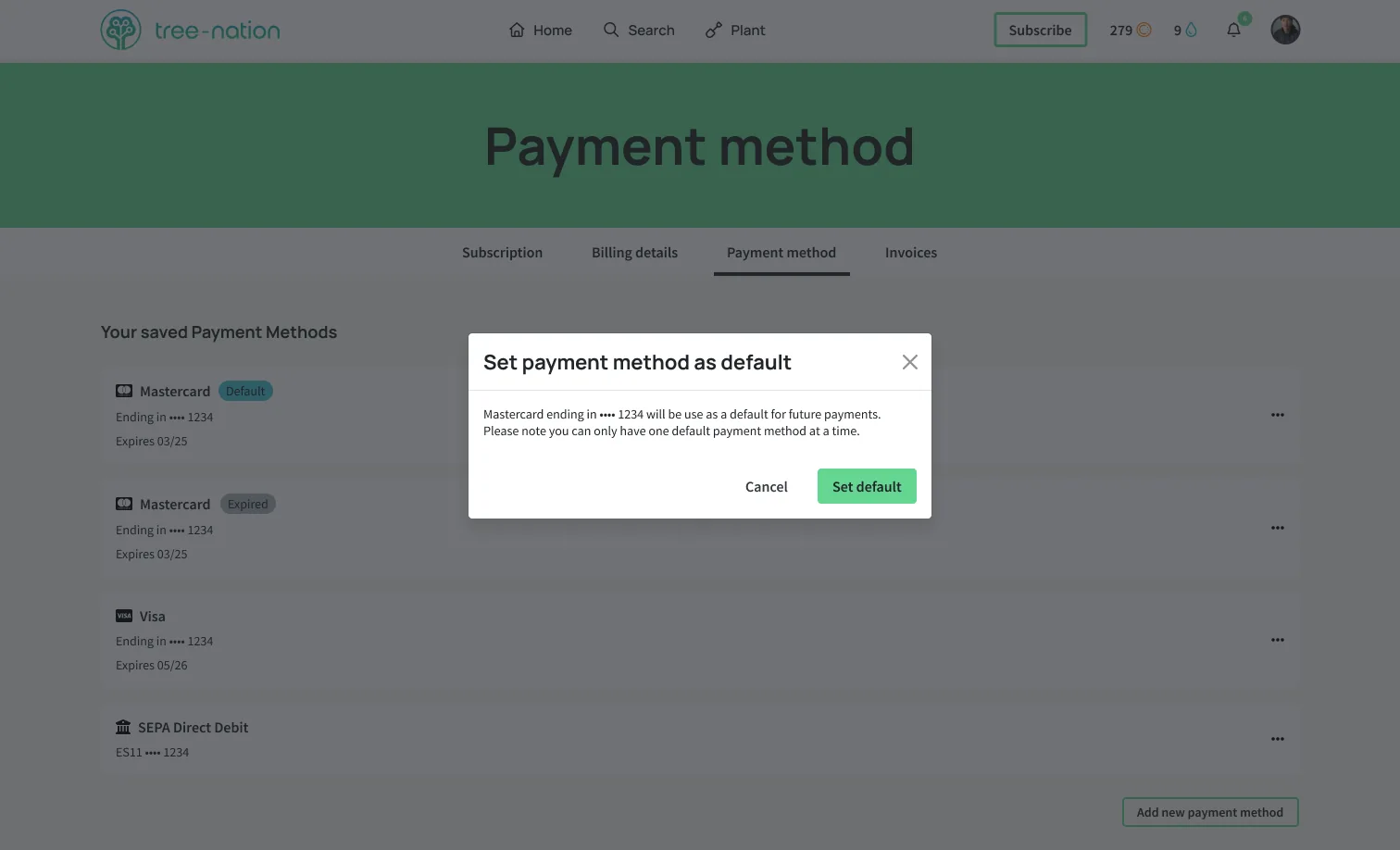

Churn was hiding

in the payment infrastructure.

A payment infrastructure overhaul that reduced churn, unlocked a new B2B market segment, and replaced manual account manager firefighting with a system that works on its own.